The pharma and healthcare sector presents a study in contrasts in terms of performance, both financially and in the BT500 ranking The pharma and healthcare sector presents a study in contrasts in terms of performance, both financially and in the BT500 ranking

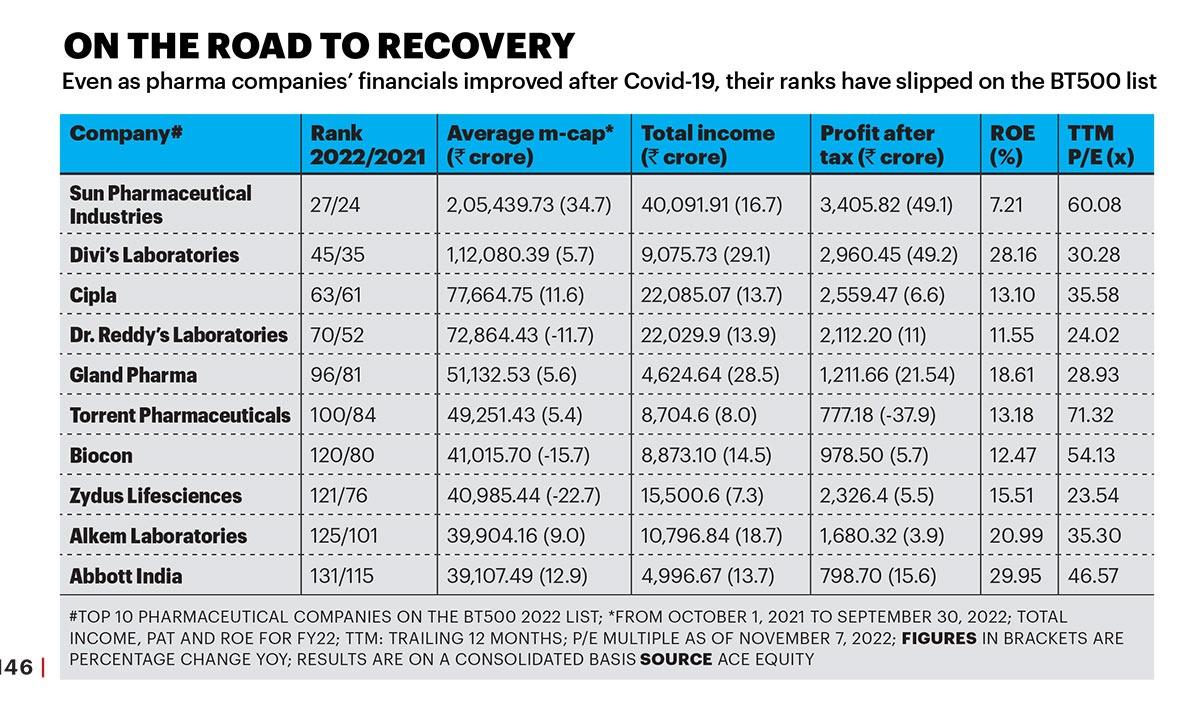

The pharma and healthcare sector presents a study in contrasts in terms of performance, both financially and in the BT500 ranking The pharma and healthcare sector presents a study in contrasts in terms of performance, both financially and in the BT500 ranking The vanishing spectre of the pandemic has left in its wake contrasting shadows in different segments of the healthcare space. While hospitals showed strong recovery due to a rise in patient footfalls and surgeries, diagnostics companies’ revenues tanked following declining Covid-19 testing in the past two quarters. And while major pharmaceutical companies are seeing revenues recover, their ranks in the BT500—based on average market capitalisation from October 2021 to September 2022—have mostly fallen below 2021.

For instance, Sun Pharmaceutical Industries, India’s largest pharma company, saw its rank slip to 27 this year from 24 in 2021. But its consolidated Q4FY22 revenues grew 10.9 per cent year-on-year (YoY) to Rs 9,386 crore. And in Q2FY23, the company recorded double-digit top line growth and strong margins driven by market share gain in India and sustained ramp-up of its global specialty business that grew 27.5 per cent. “We continue to focus on expanding our global specialty business and growing all our businesses,” Dilip Shanghvi, MD of Sun Pharma, told BT in an emailed response.

Similarly, Dr. Reddy’s Laboratories’ rank in the BT500 fell from 52 in 2021 to 70 in 2022, despite its strong performance in the past several quarters. In Q2FY23, it reported revenue growth of 11 per cent YoY. The company is currently investing in several businesses for long-term growth, including neutraceuticals, contract development and manufacturing organisation (CDMO) services, vaccines and digital healthcare platforms. “We aim to continue to deliver growth and profitability through improved execution on product development and launch, improved productivity driven by continuous improvement as well as digitalisation,” a company spokesperson told BT.

The story is similar for other companies like Divi’s Laboratories and Cipla, but there are new challenges. “During Covid-19, most segments of the pharma sector including generics, domestic formulations, APIs and CDMO saw one-off opportunities that led to robust numbers for all companies. But, in the current year, there has been an increase in overall costs in line with lower operating leverage. Going forward, normalcy would return with stability in revenues and profitability for pharma companies,” says Rajesh Pherwani, Founder and Portfolio Manager of Valcreate Investment Managers.

For diagnostics firms, the wave of windfall profits is over following reduced RT-PCR testing. In Q2FY23, Dr Lal PathLabs recorded a 24.82 per cent dip in consolidated net profit to Rs 72.40 crore in comparison to Q2FY22. The company also slipped from No. 164 in the BT500 rankings for 2021 to No. 202 this year. Similarly, Metropolis Healthcare reported a 30.69 per cent decline in consolidated net profits, from Rs 58.40 crore in Q2FY22 to Rs 40.48 crore in Q2FY23. Its overall revenue fell 0.8 per cent YoY, and Ebitda margin dropped over 350 basis points (bps) YoY. Metropolis’s BT500 rank fell from No. 249 in 2021 to No. 308 in 2022.

According to a recent report by Antique Stock Broking, margins of the diagnostics industry reported during FY21 at the peak of Covid-19 will not be repeated anytime soon. Companies will record long-term revenue growth of 10-12 per cent, much lower than around 15 per cent CAGR seen in the past few years. Another report from Credit Suisse noted that Ebitda margins of Dr Lal and Metropolis have already declined by 300 bps (vs pre-Covid-19) to 23 per cent, and Credit Suisse’s analysts expect them to contract further by 300-400 bps.

Meanwhile, the hospitals sector fared well in the BT500 rankings this year due to improvement in non-Covid patient footfalls, resumption of medical tourism, increase in routine surgeries and expansion by major players. Narayana Hrudayalaya rose in the rankings from No. 298 in 2021 to No. 281 in 2022. Fortis Healthcare remained stable with one position down (from No. 222 in 2021 to No. 223 in 2022). And Max Healthcare’s ranking improved from No. 184 in 2021 to No. 138 in 2022. In Q2FY23, Max reported consolidated operating profit of Rs 344.74 crore (compared to Rs 270.36 crore in Q2FY22), with overall occupancy at 78 per cent versus 74 per cent in Q1 on seasonality.

Per a report by credit rating agency CareEdge in June 2022, hospitals’ revenue growth was estimated at 15 per cent for FY22 due to higher occupancy, better patient mobility on account of ‘living with Covid-19’ policies, and resumption of non-Covid surgeries. Comparatively, in FY21, the segment had reported subdued revenue growth of 7 per cent, primarily due to the lockdowns, which affected patient mobility. “Hospitals are structurally well-placed with momentum expected to continue from a robust Q1FY23. The momentum is likely to be driven by sequential in-patient volume and thus, higher in-patient conversion. One important lever could be incremental elective surgeries, due to continuum of pent-up demand, post-Covid-led complications and higher international patients mix,” says Siddhant Khandekar, Analyst at ICICI Securities Research.

Looking Ahead

Despite the contrasts, the future looks promising for the overall industry. Arvind Sharma, Partner at Shardul Amarchand Mangaldas & Co, explains why. “Several new products are lined up for approvals, and the pharma sector is securing benefits including on account of digitisation, use of AI and increased R&D. All of this, and recent changes in the global economic and political situation, should enable continuity of excellent performance in the Indian pharma sector, and we have a positive outlook for growth in the next year as well,” says Sharma, who tracks the pharma sector.

Experts say the companies to watch out for next year are Fortis, Sun Pharma, JB Chemicals & Pharmaceuticals, Torrent Pharmaceuticals, Abbott and Dr. Reddy’s. Sun Pharma is expected to show strong growth in the US specialty drugs business (specialty drugs are copies of biologics, which are derived from living cells). Analyst firm Nirmal Bang has said that JB Chemicals’ revenue is expected to grow 32.2 per cent YoY in the next quarter mainly due to 45 per cent YoY growth in the domestic market.

Torrent is expanding with mergers and acquisitions and investments in diagnostics. It acquired Curatio Healthcare in September 2022 for Rs 2,000 crore, which is its most expensive deal so far. This acquisition, the company has said, is expected to enhance its presence in the cosmetic dermatology market. As for Dr. Reddy’s, analysts continue to be positive on the stock, given the expected growth momentum in its branded generics business, strong product launch run-rate in the US, enhanced focus on margins, and attractive valuations.

Another company to watch out for, analysts say, is Piramal Pharma Ltd (PPL). After its demerger from parent company Piramal Enterprises, PPL is now a large listed entity in the pharma sector. Having sold its domestic formulations business in 2010 (which comprised around 55 per cent of FY10 sales of Rs 3,670 crore) to Abbott, Piramal has rebuilt its pharma business to Rs 6,700 crore in sales in FY22. The billion-dollar-revenue mark appears within touching distance now.

While recent times have seen mixed fortunes for the pharma and healthcare sector, the industry appears to be moving in the right direction in terms of growth.

@neetu_csharma

Copyright©2023 Living Media India Limited. For reprint rights: Syndications Today