Illustration by Raj Verma Illustration by Raj Verma

Illustration by Raj Verma Illustration by Raj Verma In August, HDFC Life, the fastest-growing private sector life insurance company, entered the coveted Nifty-50, the flagship index of the National Stock Exchange tracked by global investors. The newly listed private insurer is now rubbing shoulders with the likes of HDFC Bank, ICICI Bank, Axis Bank and Kotak Mahindra Bank. Soon, Life Insurance Corp of India (LIC) is also set to debut on Dalal Street, which, according to experts, could be dubbed as Indias ARAMCO moment (the Saudi Arabian oil major recently turned out to be the company with the largest market cap globally). In fact, with a likely valuation of over Rs 10 lakh crore, LIC will only be second to Reliance Industries in market cap (Rs 14 lakh crore), ahead of biggies such as TCS, HUL and Infosys.

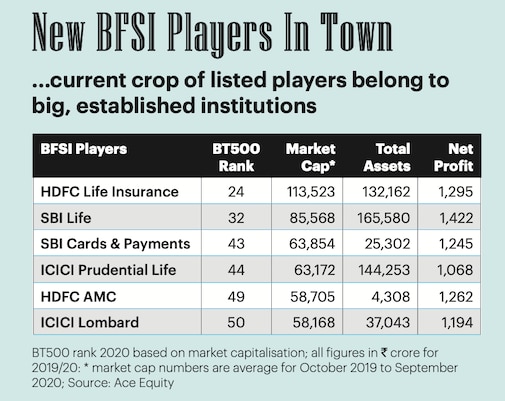

The BFSI - banking, financial services and insurance - game is changing the stock market. For decades, banks and non-banking financial firms (NBFCs) ruled the stock market in terms of market cap and investors interest. However, the last few years have seen increasing number of listings from life insurance, general insurance, mutual fund asset management companies (AMCs), pure play credit card companies and small finance banks. Business Today's listing of top 500 companies in India captures the trend. HDFC Life, for instance, has gone up eight ranks, from 32 to 24. A pure play credit card company, SBI Cards & Payments, which got listed this year, has been ranked 43rd in the very first year. HDFC AMC has improved its ranking from 75th to 49th position. Small finance banks have also found a place among the top 100 companies.

The Positives

So, what is working in their favour?

A well-established brand name, global tie-ups, a stable business model with existing operation of 15-20 years, profitability, and a huge opportunity to grow the business are some of the reasons for investor interest in these companies. "We have now widened and deepened customer offerings. Globally, financial services comprise deposit-taking machines, or banks, asset management companies for investments and life insurance entities for protection as well as investments," says Vimal Bhandari, a veteran in financial services, who sits on boards of RBL Bank, Piramal and DCM Shriram Group.

According to Amit Tandon, Founder and MD of proxy advisory firm IiAS, and former MD of Fitch Ratings in India, these are all professional companies with pedigree of large institutions. "In the next decade, linkages with their parents will tend to fray because of regulatory and other factors to make them truly professionally run companies," he says. Investor interest, including from global companies, also stems from the professional management and independent boards of these new listers.

The one thing common among these companies is that they all started some 15-20 years ago when the sector opened up for private participation. The first set of licences was secured by large private institutions in partnerships with global giants in mutual fund, insurance, credit card etc. For instance, from a single player (LIC) in the life insurance sector some two decades ago, there are now over two dozens. Private sector companies have also been steadily building scale. The most profitable ones, including HDFC Life, ICICI Pru Life and SBI Life, are listed on the bourses. Similarly, general insurance has two listed entities - one each from private (ICICI Lombard) and public (New India Assurance) sectors. The sector has some 34 players, including pure play health insurance providers. "We will have niche BFSI segments in future, like health insurers, getting listed in the stock market. Investors will have a choice between life, non-life and health to invest," says the CEO of a private sector life insurance firm. It's like diversifying within the sector itself. Currently, the investment in a life insurance stock generally get precedence over general insurance in terms of diversification, compared to banks and NBFCs. "Life insurance comes first when one thinks of taking insurance. So, this business has huge potential," says Mohit Mangal, Research Analyst at Anand Rathi Shares & Stock Brokers.

The largest state-owned reinsurer, GIC Re, is also listed in the market. In the mutual fund segment, UTI Mutual Fund got listed last week. HDFC AMC and Nippon Life AMC are the other two listed mutual fund houses. Market grapevine has it that SBI AMC is also firming up plans for listing. "AMC is actually a fee-based business and comes close to businesses like credit ratings," says Gaurav Jani, analyst at Centrum Broking. CRISIL and Care Ratings are currently listed. "It is a choice between AMC and credit rating for investors when it comes to investments," adds Jani.

SBI Card & Payments is the only pure play card company listed on the bourses. Similarly, there are also small finance banks, which are mostly micro finance institutions with decade of experience that have now converted into banks.

Strong Numbers

The numbers speak for themselves. In the last five years, HDFC AMC has grown its revenues at a compounded annual growth rate (CAGR) of 15 per cent to Rs 2,000 crore, with net profit showing a CAGR of 25 per cent to Rs 1,262 crore. The AMC has around 38 per cent of its AUM locked in equity schemes, while 62 per cent is parked in fixed-income instruments. "Our unique investor count stands at 56 lakh, against the industry total of 2.08 crore. So, over one out of every four mutual fund investors have invested with us," Milind Barve, MD, HDFC AMC, recently said to investors.

HDFC Life faced some initial hiccups, but later witnessed a turnaround. The credit goes to Amitabh Chaudhry, who recently left the company to head Axis Bank. In 2019/20, the company collected new business premium of Rs 17,238 crore, and had a market share of 21 per cent. The life insurer's AUM is around Rs 1.27 lakh crore, with a balance portfolio of unit-linked plans (28 per cent), participating policies (19 per cent), non-participating (41 per cent), protection (8 per cent) and annuity (4 per cent).

In its recent report, Emkay Global said HDFC Life's balanced product mix provides a cushion against any business cyclicality. "We expect margins to improve gradually with the rising share of protection plans and increasing penetration in geographies," according to the report. Dinesh Khara, the new SBI chairman, who was on the board of SBI Cards as a director, recently said the company's card business is growing faster than the industry average. This reflects in the 28 per cent year-on-year growth in card holders to 1.05 crore in 2019/20. Card spends jumped 27 per cent to Rs 1.30 lakh crore in the same period.

In the small finance banking space, Ujjivan Small Finance Bank is riding high. It reported a 49 per cent year-on-year jump in revenues to Rs 3,026 crore, while net profit rose 76 per cent to Rs 350 crore in 2019/20.

Digital Boost

Like in banking, the digitisation of offerings right from customer on-boarding to servicing is transforming business models. ICICI Lombard, for instance, issues over 96 per cent of its policies online. The insurance industry manages renewals and claim settlements online. There are now AI-enabled claim settlement engines. Public sector companies, however, have still some catching-up to do in the digitisation space.

These new businesses have huge opportunities to grow if one look at penetration levels. The share of household savings in financial assets (excluding physical assets) shows the share of mutual funds at 6 per cent and insurance at 11 per cent. Given the falling interest rates, equity as an asset class will see an exponential growth. Similarly, the penetration of life and general insurance has been in single-digits for decades. Small finance banks such as Ujjivan are operating in under-served and under-banked territories, where there is huge potential for growth.

These new business models also have their risks. For instance, SBI Cards recently saw gross NPAs doubling in the second quarter of 2020/21 because of lockdown and economic slowdown. The general insurance business of motor, fire etc is linked to the performance of the economy and the industrial sector. In its recent report, HDFC Securities cautioned that more health claims due to a second wave of Covid could result in significant increase in claims. Some companies recently exited the crop insurance business because of higher underwriting losses. Similarly, unit-linked business in life insurance depends on stock movements. During a bear phase, the return comes under pressure.

AMCs also face credit risks like in the event of the IL&FS failure. "It is difficult to manage a risk," says Jani of Centrum. This is because some of the investment grade paper became junk overnight. Small finance banks, too, have a higher reliance on unsecured products and a particular class of borrowers who are not salaried.

Investors therefore need to be careful while taking pricing bets, and invest long-term in these new businesses.

@anandadhikari

Copyright©2023 Living Media India Limited. For reprint rights: Syndications Today